Reserve with Google

Reserve with Google

Many businesses needlessly lose thousands of dollars to credit card processing fees every single year.

In many cases, these figures are in the ballpark of at least $4,000+ or more. Over a period of five years, you could be overpaying by $25,000 dollars (and likely much more than that!). This is due to having the wrong pricing model for your business as well as higher processing costs and hidden fees like international fees.

It’s exactly why we launched Yocale Pay: to reduce unnecessarily high payment processing costs.

If you’re looking to choose a payment processor (or if you’re looking to make a switch), we’ll do a comparison of the most common options to see where you might be overpaying.

Credit Card Payment Processors: Comparison Chart

1. Pricing Model: Interchange-Plus Pricing, Flat Rate or Tiered Pricing

Before you ever compare actual processing rates, the single most important thing you can do when choosing (or switching to) a payment processor is to choose the right pricing model for your business.

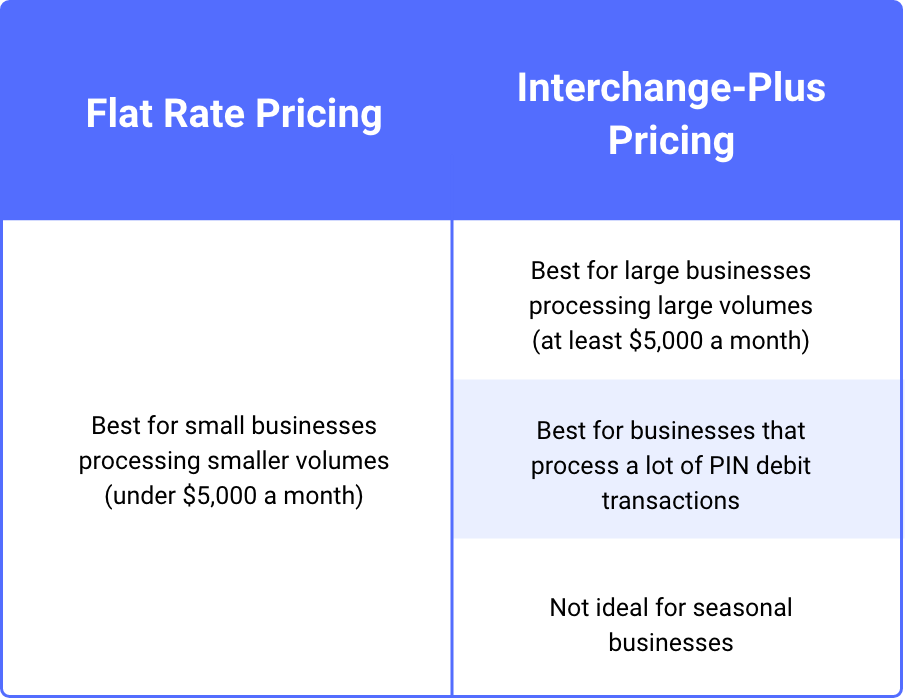

The three standard models are interchange-plus pricing, flat rate pricing and tiered pricing (although we recommend avoiding tiered pricing altogether).

In a nutshell, interchange-plus pricing charges you the true interchange fee, which actually varies based on the type of card you’re processing and the industry your business is in. If you’re paying a flat fee, you pay the same fee regardless, which can lead to overspending depending upon your business.

In the chart below, you’ll see what type of pricing model is best for your business.

2. Processing Fees

In addition to the pricing model, the next thing to consider is the processing rate.

While we acknowledge our bias, Yocale Pay offers wholesale rates, which means our rates are the lowest in the industry – regardless of whether you’re on a flat rate pricing plan or interchange-plus.

Given that most payment processors only offer a flat-rate model, the comparison below will compare flat rate pricing across several processors.

*Rates based on October 2021 data*